Most people can’t fill their full £20,000 Isa allowance each year, but there is a move that lets you use some with existing investments while protecting them from tax in the future.

It’s called a Bed & Isa and involves selling shares, funds or other investments held outside a stocks and shares Isa and buying them back inside one, so they will be shielded from tax.

Bed & Isa activity has cooled off since the big capital gains tax changes last year, but it is still a popular way to protect investments from the taxman.

But you do have to weigh up the potential CGT bill on selling your investments and investigate the costs of carrying out the deal.

Online platform Interactive Investor says its Bed & Isa transactions were down 40 per cent in the first two months of this year compared with the same period in 2024.

This time last year investors were trying to dodge swingeing cuts in April to the capital gains tax allowance, which took it down from £6,000 to £3,000, and also to the dividend tax-free allowance, which was halved to £500.

Interactive Investor also had a record-breaking summer and third quarter for Bed & Isa transactions, as investors correctly anticipated pending hikes to CGT rates in the 30 October Budget.

‘The rush to Bed & Isa came earlier than usual,’ says Myron Jobson, senior personal finance analyst at Interactive Investor. ‘But the reality is that anytime is a good time to shelter investments within the tax-efficient Isa wrapper.’

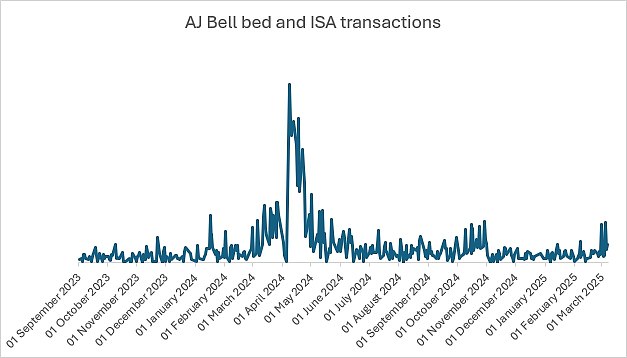

AJ Bell saw the number of Bed & Isa transactions on its platform spike in the first two weeks of 2024/25 – see the table above for activity throughout the tax year.

The platform also reports a jump of almost 300 per cent in such deals in October 2024 – in the immediate run-up to the Budget – against the year before.

The CGT rates for stocks and shares gains were raised in the Autumn Budget from 10 per cent to 18 per cent for basic rate taxpayers and from 20 per cent to 24 per cent for those paying higher rates of tax.

‘Investors have battled a triple threat of hikes in CGT rates, huge cuts to the tax-free allowances for capital gains and dividend income, and frozen tax bands,’ says Charlene Young, pensions and savings expert at AJ Bell.

‘Not only will they pay more tax on their existing gains and investment income outside of Isas, but more investors have been pushed into a higher tax bracket and rates of tax on their holdings.

‘It’s therefore no surprise that Bed & Isas remain a popular option for investors as we enter peak Isa season.’

How does a Bed & Isa work?

The process involves transferring investments held outside a Isa into one, to shield the assets and future gains and income from the taxman.

Jobson says: ‘Customers will pay a trading fee on the re-purchase, not the sale.

‘This means it’s far cheaper to Bed & Isa than to sell your investments yourself, transfer your cash into your Isa, and then repurchase the shares.

‘Customers will also pay stamp duty and market spread costs. Capital gains tax is payable on any profits above a person’s annual allowance, but moving the investments to an Isa means you won’t pay capital gains tax on those profits in future.’

Young says: ‘You’ll still be using your annual Isa allowance with a Bed & Isa deal, so keep an eye on how much of the overall £20,000 you have left.

‘You’ll also have to pay CGT on your gains over the annual tax-free amount (£3,000 for 2024/25).

‘Only investments that are traded on an exchange are eligible for Bed & Isa. That includes UK-listed and most internationally-listed shares, investment trusts, ETFs and bonds, but not investment funds (OEICs and unit trusts).’

She adds: ‘If you’re considering repositioning your portfolio or your overall asset allocation, then you’re unlikely to use a Bed & Isa if you want to buy different investments with the sale proceeds.’

How to use Bed & Isa to protect investments from tax

Rob Morgan, chief investment analyst at Charles Stanley, offers the following tips.

1) Calculate your CGT bill: A Bed & Isa is treated as a sale for CGT purposes, which means that if the gain, when added to your other gains for the tax year, exceeds the annual CGT allowance of £3,000 (in 2024/25) you will have to pay tax.

But don’t forget you can offset losses when calculating CGT liabilities and these can be harvested at the same time as gains, potentially to keep within the allowance.

2) Check the costs: There are also costs involved with a Bed & Isa. When selling and buying shares there is a difference between the buying and selling prices, known as the bid-offer spread, to be considered.

So together with dealing commission and stamp duty it means fewer shares are repurchased in the Isa than sold.

However, you’ll end up with the investments sheltered from tax on income and profits going forward so it can be a price worth paying.

3) Consider your timing: If you have sizable gains on your investments and you are going to go beyond the CGT allowance, or your income is likely to vary, it is worth considering the most opportune time to carry out a Bed & Isa.

For example, if you are planning to sell assets that have gone up in value by more than the allowance it may make sense to split this over more than one tax year.

You can choose which assets to Bed & Isa or sell and crystallise and gains or losses, and the tax year in which to do it to help minimise CGT.

Losses can also be carried forward to set against future gains, but they must be declared, which can do up to four years after the end of the tax year that you disposed of the asset.

4) Don’t forget income tax: One thing to bear in mind is that the CGT rate applied depends on your income from the tax year with the gain added on top.

Any part falling within the basic rate band is taxed at the lower rate and anything above at the higher rate.

This interaction between CGT and income tax is sometimes overlooked. If your earnings are likely to drop in a subsequent tax year it can make sense to defer any sales and Bed & Isas.

5) Involve your spouse: One other trick is to move an investment into a spouse’s name to take advantage of two CGT allowances – effectively increasing the profit you can make without tax to £6,000 assuming of course they already have no gains of their own.

It can also make sense in some situations to transfer assets in full to a lower earning husband, wife, or civil partner where they would incur less tax on a sale or a Bed & Isa.

DIY INVESTING PLATFORMS

AJ Bell

AJ Bell

Easy investing and ready-made portfolios

Hargreaves Lansdown

Hargreaves Lansdown

Free fund dealing and investment ideas

interactive investor

interactive investor

Flat-fee investing from £4.99 per month

Saxo

Saxo

Get £200 back in trading fees

Trading 212

Trading 212

Free dealing and no account fee

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.

Compare the best investing account for you

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.