Those earning a modest wage – £10,000 to £19,999 – and aged between 25 and 34, are most likely to be putting money into cash Isas, government statistics show.

Sarah Coles, head of personal finance at Hargreaves Lansdown, says: ‘Cash Isas aren’t the luxury sports cars of the financial world, exclusively for the super-rich.

‘All sorts of other people can benefit from the tax savings.’

Here’s how to check if your Isa stacks up, based on the average for your age group, emergency fund needs – and how you should save and invest into it at key moments in your life.

Under 25

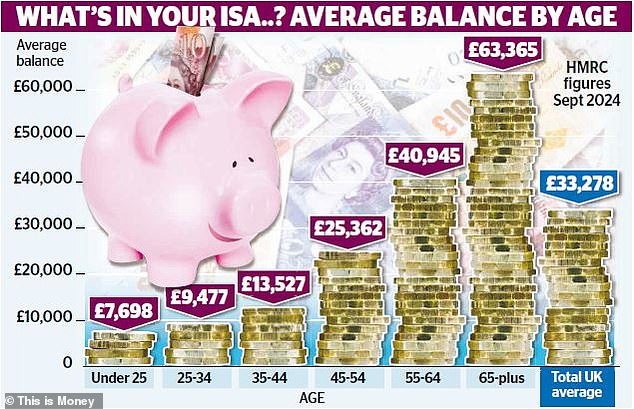

Average Isa balance: £7,698.

Ideal Isa balance: £11,420 (split between £2,760 in an easy-access cash account, £7,370 in a Lifetime Isa (Lisa) and £1,290 in a stocks and shares Isa).

Having spare money for an Isa might seem like a pipe dream right now, but getting started at this age can improve your financial resilience, and build the foundations of an impressive Isa pot.

Your balance will have to work hard if it is your only savings account and you may want to split it into a Lifetime Isa (Lisa), to save for a house deposit, a stocks and shares Isa for future growth and a cash Isa for easy-access savings.

Jonathan Watts-Lay, director of workplace financial experts Wealth at Work, believes everyone should have between three and six months of savings in an easy-access account. ‘Many people realise too late the importance of having emergency savings,’ he warns.

The average weekly spending for the under-25s is about £230 a week, government figures show, meaning you’d need £2,760 in an easy-access Isa account to cover three months of costs.

Once you’ve built up this emergency fund, extra Isa savings should go into longer-term products. If you’re hoping to buy a home, a Lisa in your 20s will benefit from a government bonus.

The average age to buy a first house is 33, and the average deposit £53,000. Split that in half, if you assume you’re buying with a partner, and you’ve got to put away £2,200 every year from graduation to 33 to make it.

To hit this target, by 25 you should have £7,370 in your account, made up of £5,568 of your own money and £1,392 of government bonus.

This assumes your money grows at 5 pc a year. You’d need to put a £116 a month into your Lisa.

Any extra money after this should go into a stocks and shares product for growth. Most allow a £25 a month minimum. Assuming you started at age 21, by 25 you could have £1,290 in this Isa if it grew by 5 per cent.

25-34

Average Isa balance: £9,477.

Ideal Isa balance: £27,023 (£7,200 in an easy-access Isa, £0 in a Lisa (assuming you are saving into a pension and have bought your first home), £19,823 in a stocks and shares Isa).

By 34, the average first-time buyer has bought a home. Bills might be higher though salaries usually are, too, and many savers will also be dealing with childcare costs (the average age to have your first child is 29, and most are done by 34).

But many of us still manage to increase Isa savings during this tricky period, with the average balance rising to £9,477.

An ideal Isa balance would be more than this, however, as you could be building up an emergency fund at the same time as paying into a stocks and shares Isa.

Taking the emergency fund first, you’re likely to need more at this age. Average household expenditure drops in our 30s, to £200 a week, but your household has likely grown, so you need to cover dependants’ emergency costs, too.

The Government’s household spending survey shows household weekly spending is £600 a week, so for three months’ expenditure you’d need more than £7,200 in an easy-access Isa account.

You may have emptied your Lisa for a deposit on a first home. Only the self-employed are likely to still be using this as the most efficient vehicle for retirement.

Otherwise you should be prioritising pension savings as you’ll receive tax relief and an employer contribution.

Your stocks and shares Isa should be growing. If you’ve stopped paying into the Lisa, you could divert the £116 a month you were paying into it into stocks and shares, while continuing with the regular £25 a month.

The two together – £141 a month – should help your stocks and shares Isa grow. Our calculations show that if you did this and your Isa grew by 5 pc on average a year, you’d have nearly £20,000 in your stocks and shares Isa by age 34.

35-44

Average Isa balance: £13,527.

Ideal Isa balance: £55,094 (£9,394 in an easy-access cash Isa, £0 in a Lisa, £45,700 in a stocks and shares Isa).

Earning potential rises but costs may rise, too, including paying for children to go to university while also paying your mortgage.

The average balance rises only a little while in this age bracket – to £13,527. You’d be able to increase your Isa balance more, though, if you kept your savings from the previous decade on track.

Our figures assume that you don’t take out money from your emergency cash Isa – or replace it if you do – and keep contributions to your stocks and shares Isa the same.

At 5 pc growth, with the same £1,692 a year put into the stocks and shares Isa each year, you’d have £45,700 by the age of 44.

Your emergency costs Isa, will be worth £9,394 if your money is gaining 3 per cent interest.

45-54

Average Isa balance: £25,362.

Ideal Isa balance: £284,038. (£113,848 in an easy-access cash Isa, £0 in a Lisa, £170,190 in a stocks and shares Isa).

The average age to receive an inheritance is 44, so you might find this is a time when you use your Isa allowance to the max.

Sarah Coles says many people this age use a cash Isa to park an inheritance ‘until they feel emotionally ready’. For those who go on to invest, they can transfer it to a stocks and shares Isa.

We see the impact of inheritance, plus falling costs as children leave home, in the increased average Isa balance for the age group – £25,362. But our ideal Isa balance is higher than this.

The average legacy is more than £300,000, which could turbo-charge your Isa savings.

Assuming that this inherited money is used to max out your Isas each year between the ages of 45 and 54, you could end up with substantial amounts in both your cash and stocks and shares Isas.

Assuming you split your Isa allowance equally between cash and stocks and shares, you’d end up with £283,000 – more than ten times the average. This assumes 5 per cent growth on investments and 3 per cent on cash savings.

55-64

Average Isa balance: £40,945.

Ideal Isa balance: £403,615 (£148,546 in your cash Isa, £255,069 in your stocks and shares Isa).

On average, Isa balances rise again at this age, reflecting the passing of time on investments, continued employment and the impact of inheritance.

But with the state pension age rising to 67 for those born on or after April 1, 1960, anyone wishing to retire before this age may be spending Isa savings to bridge a gap in income.

If you continue to add the same monthly amount into Isas as in your 20s (£141 a month), and it is all added into your stocks and shares Isa, you will still have more than £250,000 by age 64.

Your cash Isa will also grow even if you don’t add to it, up to nearly £150,000.

65-plus

Average Isa balance: £63,365.

Ideal Isa balance: £486,887(£293,069 stocks and shares, £193, 818 (if no withdrawals).

Balances continue to rise. But if you’ve reached this age with a healthy Isa pot, it might be time to consider giving some of it away.

Everyone should weigh up the potential cost of future care and life expectancy, but there is an argument for running down your Isas at this point by giving cash to dependants, especially since you’ll no longer be able to pass your pension down to them inheritance tax-free.

But you will also need money to live on, so it is a balancing act.

Here, we are assuming you take £10,000 a year from your Isa to give to children or grandchildren, with your money not in line for inheritance tax if you live seven years after giving it away.

Even if you do this and live on your pensions, your Isa would be larger than it was at age 64 by the time you’ve reached 75.

A £255,000 stocks and shares Isa with £10,000 withdrawn from it annually but with a 5 per cent growth rate would be worth more than £293,000 by the end of a ten-year period.

Your total Isa pot could be almost £500,000, including the emergency fund in cash Isas.

As the calculations above show, even someone with an average income, outgoings and rate can build a bigger pot than you think.

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.